Finance · United States 🇺🇸 · Tax Year 2026

US Federal Income

Tax 2026: IRS Brackets,

Rates & Calculator

Tax year 2026 covers income you earn from January 1 through December 31, 2026. What’s being withheld from your paycheck right now — the PAYE deductions showing up every two weeks — is based on the 2026 tax brackets and the 2026 standard deduction. Understanding these numbers tells you whether your withholding is accurate, how a raise affects your take-home, and what steps you can take before December 31 to reduce your tax bill.

Two things make 2026 different from recent prior years. First, the One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, permanently locked in the lower tax rates that were temporary under TCJA — removing years of uncertainty. Second, 2026 brings genuinely new benefits: a charitable deduction for non-itemizers, higher HSA limits, and a new 401(k) super catch-up for ages 60–63. Every figure in this guide is sourced from IRS Revenue Procedure 2025-32.

What’s New for Tax Year 2026

The OBBBA made the lower TCJA tax rates permanent — so the brackets themselves are stable. What changed for 2026 are the inflation-adjusted thresholds and several new provisions that didn’t exist before.

✦ Key Changes for Tax Year 2026

Source: IRS Revenue Procedure 2025-32 and One Big Beautiful Bill Act (OBBBA, P.L. 119-21)

The most significant genuinely new benefit for most taxpayers: the charitable deduction for non-itemizers. Starting in 2026, even if you take the standard deduction, you can separately deduct up to $1,000 in cash donations (single) or $2,000 (MFJ) to qualifying 501(c)(3) organizations. This is the first time in decades that non-itemizers get any charitable deduction — and it applies to any cash donation you make in 2026.

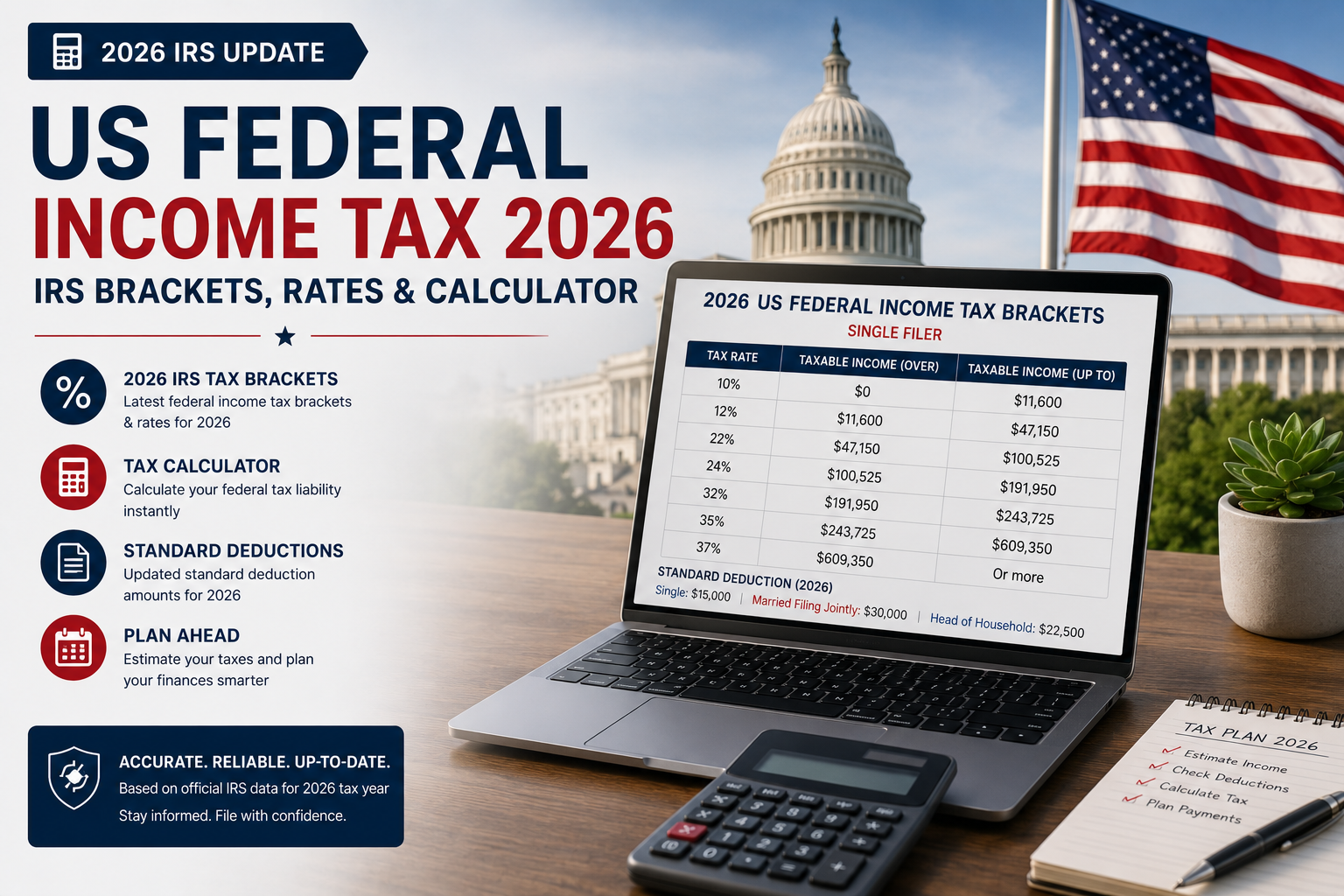

2026 Federal Tax Brackets — All Filing Statuses

These are the official 2026 federal income tax brackets from IRS Revenue Procedure 2025-32. Rates are marginal — each applies only to income within that band, not your entire income.

Single Filers — 2026

10% on the first $12,150 of taxable income. Every single filer pays this rate on their initial earnings above zero. After the $16,100 standard deduction, a single filer earning $28,250 gross has $12,150 of taxable income — all at 10%, paying $1,215 in federal tax.

Tax: $1,215.00

($12,150 × 10%)

12% on taxable income $12,151–$49,050. At $60,000 gross income, taxable income is approximately $43,900 after the standard deduction — most of it in this bracket. Maximum tax within this bracket: $4,428.

Tax: $4,428.00

($36,900 × 12%)

Effective at $65k: ~9.5%

22% on taxable income $49,051–$104,800 — a $55,750 range. At $80,000 gross, only about $14,750 falls in this bracket after the standard deduction. Your marginal rate is 22%, but your effective federal rate on the full $80,000 is around 12–13%.

In 22% bracket: ~$14,750

Tax here: ~$3,245

Eff. fed rate: ~12.3%

24% on taxable income $104,801–$200,200. At $150,000 gross, taxable income is $133,900 after the standard deduction — putting about $29,100 into this bracket. Effective rate at $150,000 is approximately 18–19%, not 24%.

Taxable: ~$133,900

In 24% bracket: ~$29,100

Eff. rate: ~18%

32% on $200,201–$253,750. 35% on $253,751–$638,400. 37% above $638,400. Only the income within each band is taxed at that rate. On $300,000 gross, approximately $30,000 falls in the 32% bracket and around $30,000 in the 35% bracket. Effective federal rate at $300,000: approximately 26–28%.

Eff. rate: ~27%

Marginal rate: 35%

37% starts: $638,400

All Filing Statuses — 2026 Bracket Comparison

| Rate | Single | Married Filing Jointly | Head of Household | MFS |

|---|---|---|---|---|

| 10% | $0–$12,150 | $0–$24,300 | $0–$17,250 | $0–$12,150 |

| 12% | $12,151–$49,050 | $24,301–$98,100 | $17,251–$65,650 | $12,151–$49,050 |

| 22% | $49,051–$104,800 | $98,101–$209,600 | $65,651–$104,800 | $49,051–$104,800 |

| 24% | $104,801–$200,200 | $209,601–$400,400 | $104,801–$200,200 | $104,801–$200,200 |

| 32% | $200,201–$253,750 | $400,401–$507,500 | $200,201–$253,750 | $200,201–$253,750 |

| 35% | $253,751–$638,400 | $507,501–$765,000 | $253,751–$638,400 | $253,751–$382,500 |

| 37% | Above $638,400 | Above $765,000 | Above $638,400 | Above $382,500 |

Calculate Your 2026 Federal Tax — Free

Enter your income, filing status, and deductions. Get your exact 2026 federal tax liability, effective rate, and monthly take-home — no signup required.

Use the Free Tax Calculator →The Bracket Myth That Costs Taxpayers Money

The most persistent misconception in US personal finance: “If my income pushes me into a higher bracket, I’ll take home less.” This is completely false — but it causes real harm when people turn down raises or bonuses to avoid crossing a threshold.

❌ The Myth vs ✅ How Brackets Actually Work

❌ What People Believe

If my income crosses into the 22% bracket, my entire income gets taxed at 22%. A raise that pushes me over $49,050 could leave me worse off financially.

✅ How It Actually Works

Only the dollars above $49,050 are taxed at 22%. The first $12,150 stays at 10%, the next $36,900 stays at 12%. A raise always increases take-home pay — without exception.

Standard Deduction 2026

The standard deduction is the amount subtracted from your gross income before calculating your federal tax. Approximately 90% of US taxpayers claim it — it’s simpler and, for most people, larger than itemizing individual deductions.

| Filing Status | 2025 Amount | 2026 Amount | Increase |

|---|---|---|---|

| Single / MFS | $15,750 | $16,100 | +$350 |

| Married Filing Jointly | $31,500 | $32,200 | +$700 |

| Head of Household | $23,625 | $24,150 | +$525 |

Additional Standard Deduction — Age 65+ and Blind

Taxpayers who are 65 or older or legally blind get an additional amount on top: $2,000 for single filers per qualifying condition; $1,600 per eligible spouse for married filers. A 68-year-old single filer’s total standard deduction in 2026 is $16,100 + $2,000 = $18,100.

Senior Deduction — $6,000 for Age 65+ (OBBBA, 2025–2028)

Taxpayers age 65 and older can claim a separate $6,000 deduction through tax year 2028. This is in addition to everything above. It phases out at 6% of income above $75,000 (single) or $150,000 (MFJ). At $175,000 single income it phases out completely. Claim it on Schedule A or as an above-the-line adjustment — your tax software will handle this automatically.

Take-Home Pay at Every Income Level — 2026

These figures show federal income tax only — not state income tax, which ranges from 0% (Texas, Florida, Nevada, Washington, etc.) to over 13% (California). FICA taxes are shown separately below. All calculations use the standard deduction.

| Gross Income | Taxable Income | Federal Tax | After-Tax | Monthly Net | Eff. Rate |

|---|---|---|---|---|---|

| Single Filer — 2026 | |||||

| $40,000 | $23,900 | $2,625 | $37,375 | $3,115 | 6.6% |

| $60,000 | $43,900 | $5,025 | $54,975 | $4,581 | 8.4% |

| $80,000 | $63,900 | $8,910 | $71,090 | $5,924 | 11.1% |

| $100,000 | $83,900 | $13,310 | $86,690 | $7,224 | 13.3% |

| $150,000 | $133,900 | $24,892 | $125,108 | $10,426 | 16.6% |

| $200,000 | $183,900 | $36,892 | $163,108 | $13,592 | 18.4% |

| Married Filing Jointly — 2026 | |||||

| $80,000 | $47,800 | $5,250 | $74,750 | $6,229 | 6.6% |

| $120,000 | $87,800 | $10,050 | $109,950 | $9,163 | 8.4% |

| $150,000 | $117,800 | $15,620 | $134,380 | $11,198 | 10.4% |

| $200,000 | $167,800 | $26,620 | $173,380 | $14,448 | 13.3% |

| $300,000 | $267,800 | $49,784 | $250,216 | $20,851 | 16.6% |

Federal income tax only. Excludes state taxes and FICA. Standard deduction applied. For personalised results including FICA, state tax, and deductions, use the free federal income tax calculator.

FICA — Social Security & Medicare Taxes 2026

FICA comes off every paycheck alongside federal income tax. The rates haven’t changed for 2026, but they’re a significant part of your total federal burden that the bracket tables don’t show.

| FICA Component | Employee Rate | 2026 Wage Limit | Max Employee Cost | Employer Also Pays? |

|---|---|---|---|---|

| Social Security | 6.2% | $176,100 | $10,918.20 | Yes — matches 6.2% |

| Medicare | 1.45% | No cap | Unlimited | Yes — matches 1.45% |

| Additional Medicare | 0.9% | $200k (single) / $250k (MFJ) | On excess only | No — employee only |

| Self-Employed (SE Tax) | 15.3% combined | $176,100 for SS portion | SS max: $21,836.40 | Deduct half on return |

On an $80,000 salary: Social Security = $4,960 (6.2% × $80,000). Medicare = $1,160 (1.45% × $80,000). Total FICA = $6,120/year ($510/month). Add this to the $8,910 in federal income tax from the table above: total federal burden = $15,030, or 18.8% of gross. Your employer pays a matching $6,120 that doesn’t appear on your payslip but represents a real employment cost.

Capital Gains Tax Rates 2026

Short-term gains (assets held one year or less) are taxed at your ordinary income rate — the same brackets above. Long-term gains (held more than one year) receive preferential rates:

| Long-Term Rate | Single Filers | Married Filing Jointly | Head of Household |

|---|---|---|---|

| 0% | Up to $49,050 | Up to $98,100 | Up to $65,650 |

| 15% | $49,051–$541,200 | $98,101–$610,050 | $65,651–$573,500 |

| 20% | Above $541,200 | Above $610,050 | Above $573,500 |

The 0% rate is a genuine planning opportunity. If your total 2026 taxable income — including the gains — stays below $49,050 as a single filer, you pay zero federal tax on long-term capital gains. This applies to early retirees, part-year workers, and anyone in a low-income year who holds appreciated investments.

Key Tax Credits for 2026

| Credit | 2026 Amount | Who Qualifies | Refundable? |

|---|---|---|---|

| Child Tax Credit | $2,000/child | Children under 17; phase-out $200k single / $400k MFJ | Partially (ACTC up to $1,700) |

| Earned Income Tax Credit (EITC) | Up to $8,231 | Low-to-moderate earned income; income limits by family size | Yes — fully refundable |

| Child & Dependent Care Credit | 20–35% of expenses | Working taxpayers with qualifying dependents | No |

| American Opportunity Tax Credit | Up to $2,500/student | First 4 years higher education; $80k/$160k phase-out | 40% (up to $1,000) |

| Saver’s Credit | 10–50% of contributions | Low/moderate income retirement savers | No |

| Electric Vehicle Credit | Up to $7,500 | New qualifying EVs; income and price limits | No (point-of-sale transfer) |

| Home Energy Credit (25C) | Up to $3,200 | Qualifying home energy efficiency improvements | No |

Retirement Contribution Limits 2026

| Account Type | 2026 Limit | Catch-Up (50+) | Special Catch-Up (60–63) | Tax Treatment |

|---|---|---|---|---|

| 401(k) / 403(b) / 457 | $23,500 | +$7,500 = $31,000 | +$11,250 = $34,750 | Pre-tax or Roth |

| Traditional / Roth IRA | $7,000 | +$1,000 = $8,000 | N/A | Pre-tax (traditional) or after-tax (Roth) |

| SIMPLE IRA | $16,500 | +$3,500 = $20,000 | N/A | Pre-tax |

| HSA (self-only) | $4,400 | N/A — age 55+ add $1,000 | N/A | Triple tax-advantaged |

| HSA (family) | $8,750 | N/A — age 55+ add $1,000 | N/A | Triple tax-advantaged |

| FSA (health) | $3,400 | N/A | N/A | Pre-tax; use it or lose it (with carryover) |

The new super catch-up for ages 60–63 is one of OBBBA’s most valuable benefits. Instead of the standard $7,500 catch-up, employees aged exactly 60, 61, 62, or 63 can contribute an additional $11,250 in 2026 — bringing the total 401(k) limit to $34,750. This is specifically for the four-year window, not ongoing. At age 64, the catch-up reverts to $7,500.

Filing Status — Which One Saves You More

Worked Example: $80,000 Single Filer, Tax Year 2026

Who Needs to Know This

Checking Current Paycheck Withholding

Your W-4 tells your employer how much to withhold. If you had a life change in 2025 or 2026 — marriage, divorce, new child, new job, side income — your withholding may be off. Use the IRS Tax Withholding Estimator at irs.gov to check, then submit a new W-4 if needed. Too little withholding means a tax bill in April 2027. Too much means you gave the IRS an interest-free loan all year.

Evaluating a Job Offer or Raise

A raise from $75,000 to $85,000 means $10,000 of additional income taxed at 22% — you keep $7,800 after federal income tax (plus FICA). State tax reduces that further depending on where you live. Use the free calculator to see the real take-home on any offer before you negotiate.

Self-Employed or Freelancer

As a 1099 worker, you owe quarterly estimated tax payments. For 2026, they’re due April 15, June 16, September 15, 2026, and January 15, 2027. Missing payments triggers a penalty. Your tax bill includes both income tax and 15.3% self-employment tax. Explore the USA financial calculators hub including the 1099 and self-employment tax tools.

Planning Before December 31, 2026

Most tax-reducing actions must happen before December 31, 2026. 401(k) salary deferrals, HSA contributions through payroll, tax-loss harvesting, charitable donations to qualify for the 2026 non-itemizer deduction — all require action this calendar year. IRA contributions can wait until April 15, 2027 but everything else closes December 31.

5 Federal Tax Mistakes That Cost Americans Money

Using the wrong filing status

Head of Household gives you a $24,150 standard deduction vs $16,100 for Single — a $8,050 difference worth $1,771 in tax at the 22% rate. Single parents who supported a qualifying dependent and paid more than half the household costs likely qualify for HoH. Many file as Single by default and overpay every year. Check the IRS HoH criteria before your next return.

Not adjusting withholding after a life change

Getting married, having a child, getting divorced, starting a second job, or earning significant investment income all change your tax liability. Your old W-4 may no longer match. The IRS Tax Withholding Estimator at irs.gov shows your estimated liability for 2026 and tells you whether to adjust. A new W-4 to your employer takes five minutes and prevents an April 2027 surprise.

Missing the new charitable deduction for non-itemizers

Starting in tax year 2026, if you take the standard deduction, you can also separately deduct up to $1,000 (single) or $2,000 (MFJ) in cash donations to qualifying charities. This is genuinely new — it didn’t exist before 2026. Keep records of any cash donations you make this year. Your tax software will include a line for it when 2026 returns open.

Not using the 0% capital gains rate in low-income years

If your 2026 taxable income (including gains) stays below $49,050 as a single filer, long-term capital gains are federally tax-free. Early retirees, those between jobs, or anyone with a low-income year can strategically realize appreciated investment gains at 0%. Many people in this situation don’t realize the 0% rate exists and wait unnecessarily to sell appreciated assets.

Ignoring the super catch-up for ages 60–63

If you turned 60, 61, 62, or 63 in 2026, your 401(k) catch-up limit is $11,250 — not $7,500. That’s an extra $3,750 of pre-tax contribution available this year (and only during this four-year window). At a 22% marginal rate, that additional $3,750 saves $825 in federal income tax. Contact your HR or payroll department to increase your deferral before December 31.

Pro Tips to Reduce Your 2026 Federal Tax Bill

Frequently Asked Questions — US Federal Income Tax 2026

Final Notes

Tax year 2026 is the first full year under a permanently stable federal tax code. The OBBBA removed the uncertainty of expiring provisions that loomed over every financial plan since 2018. The brackets you see here will remain the structure for the foreseeable future — only the inflation adjustments will shift thresholds year to year.

Two actions worth taking before December 31, 2026. First, review your 401(k) contribution — especially if you’re aged 60–63, where the $11,250 super catch-up represents a significant one-time window. Second, make any cash charitable donations you plan to make this year, and keep records. The new $1,000/$2,000 non-itemizer deduction is available for the first time in 2026 — it requires actual 2026 payments to qualifying charities to claim.

For everything else — calculating your withholding, comparing job offers, estimating quarterly payments — the free calculator handles the maths so you don’t have to.

Calculate Your 2026 Federal Tax — Free

Enter your income, filing status, and deductions. Get your exact 2026 federal tax, effective rate, and take-home pay. Updated for all OBBBA and IRS Rev. Proc. 2025-32 changes. No login.

Open Free Tax Calculator →